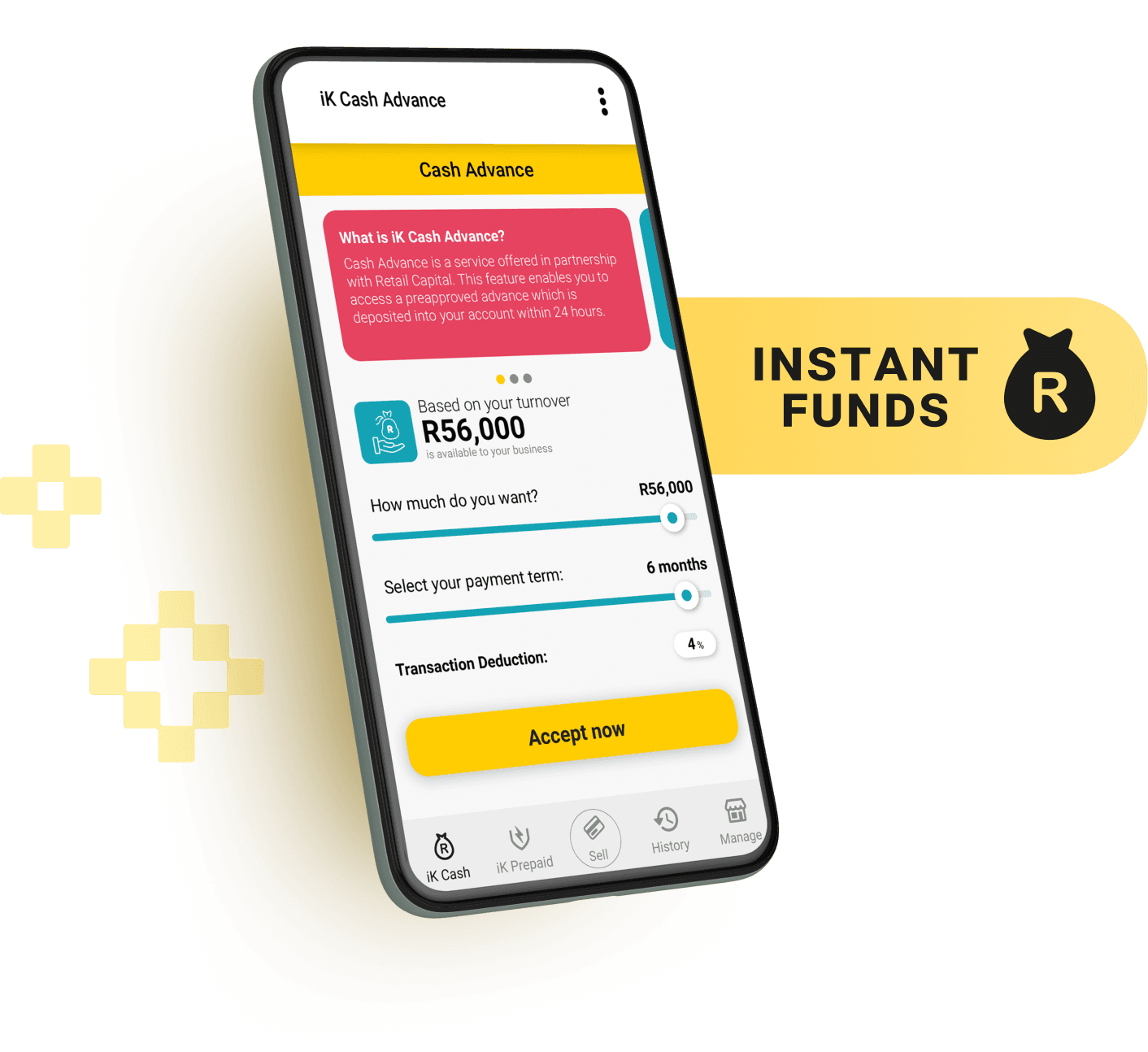

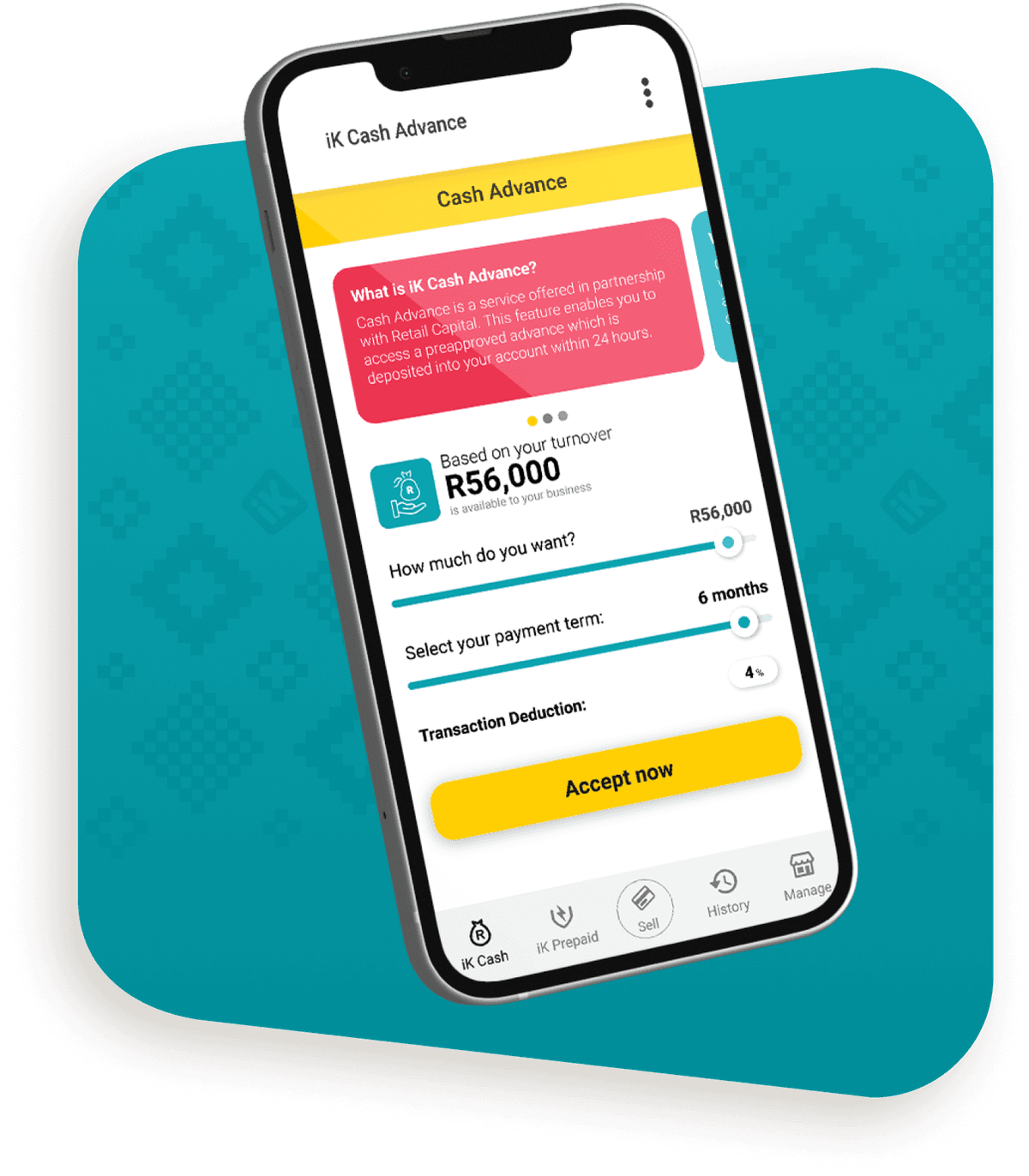

What is iK Cash Advance?

iK Cash Advance is a business cash advance built around how your business earns. If you qualify, you can access upfront funding and pay it back through a percentage of your future card sales.

That means you pay more when business is busy and less when sales are slower. There’s no fixed monthly repayment, no compound interest and no long application process. Before you accept, you’ll see your offer amount, repayment percentage and total amount payable upfront.

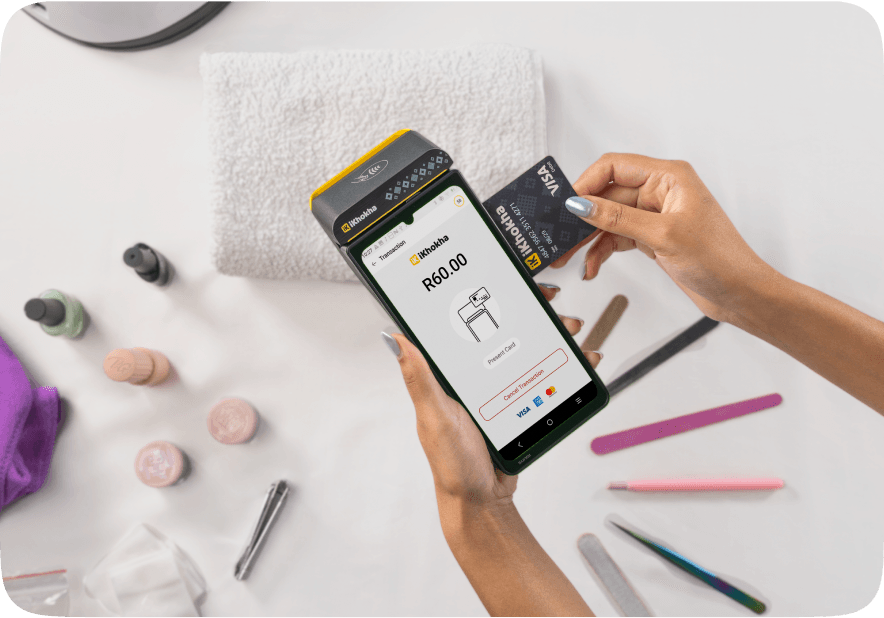

It works best for businesses that take card payments often, like shops, restaurants, salons, spaza shops and online stores, because you pay it back through your card sales.

To qualify, you need to:

- Be an active iKhokha merchant for at least 6 consecutive months.

- Make more than R2 500 in sales per month.

167%

Merchants saw 167% in sales over 3 months after taking an iK Cash Advance.

Feel inspired

“iKhokha helped me with instant cash injections in the form of iK Cash Advance. Sometimes, you lose hope in business when you don’t have enough capital, and iKhokha supported me so much during that time.”

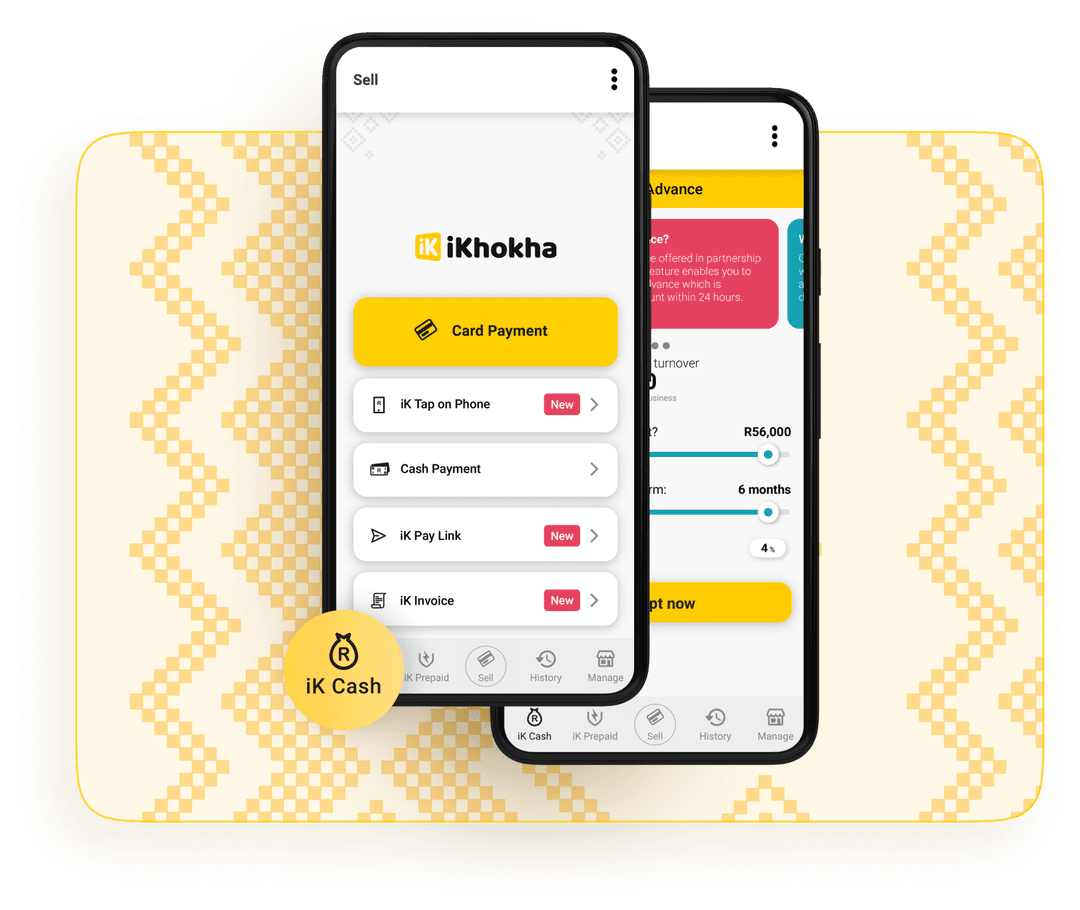

How to check your iK Cash Advance offer

You can only view Cash Advance offers on the iKhokha App.

Product Features

- 1Sign up to create your free iKhokha profile.

- 2Download the iKhokha App from your app store and login using your profile's details.

- 3Tap “Cash Advance” to see if you qualify and how much you could get.

- 4Accept an offer you’re happy with to get funding in 24 hours.

- 5Keep a healthy repayment history to qualify for more funds with an iK Cash Advance Top Up.

Easy repayments

Your repayments move with your sales. Every time a customer pays by card, a small percentage goes towards your iK Cash Advance. On busier days, you pay back a little more. On quieter days, you pay back less. That means you’re not locked into a fixed monthly repayment when business slows down.You’ll see your repayment percentage and total amount payable before you accept your offer.

FAQs

Your business must be trading for 6 months consecutively and have a minimum monthly turnover of R2 500 in order to qualify. Ts and Cs apply.

A business cash advance gives you upfront funding that is repaid through a percentage of your future sales. With iK Cash Advance, eligible iKhokha merchants can access funding and repay it through daily card sales.

You can use it for whatever your business needs. No one knows your business better than you, so the choice is yours.

Disbursement takes place on the first business day after signing. Your funds should be in your bank account within 24 hours of disbursement (subject to your bank’s turnaround times).

Payment is made via split processing: a specified percentage of your daily turnover will be used to pay back your advance.

Need help?

Get help instantly on WhatsApp, our chatbot Kelly, or by requesting a callback.

You can also call 087 222 7000 or email support@ikhokha.com